Annual Update 1997

Economic Forces that shape Montgomery County

NOTE: Detailed summary February, 1998

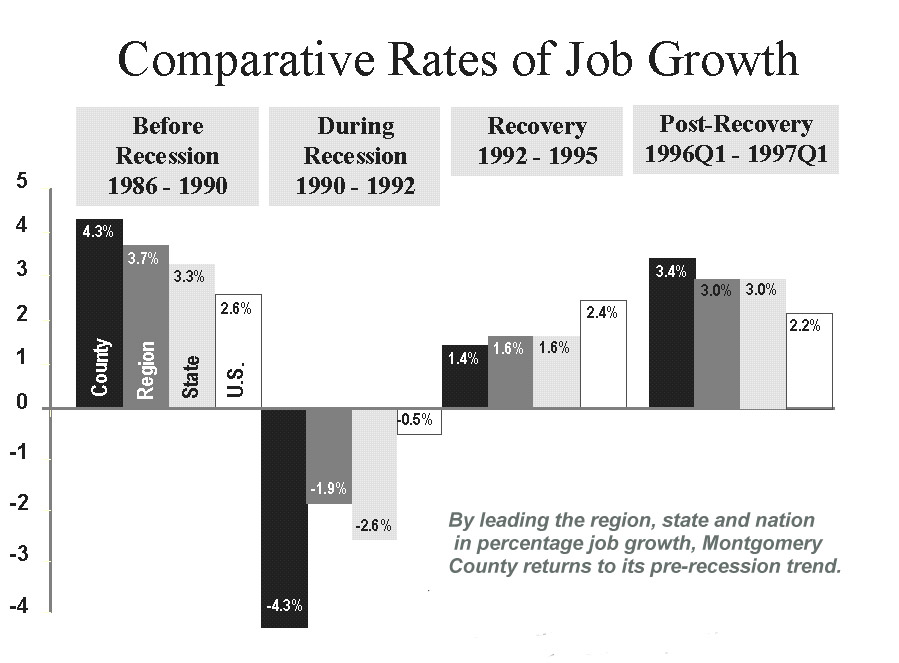

Job Growth

- Montgomery

County is adding jobs at an accelerating rate. Montgomery County's 3.4 percent annual rate of job growth

is now faster than the region's, the state's, and the

nation's. The County's recovery from the 1990-92 recession

had been fairly slow, with job growth increasing by

only 1.4 percent in three years.

Comparative Rates of Job Growth - In actual numbers, the County is adding more new jobs than any County in the Washington/Baltimore area, save one. Montgomery County added 13,000 new jobs between the first quarter of 1996 and the first quarter of 1997. The County added 11,000 jobs between the second quarters of 1996 and 1997. This is second only to Fairfax County in the region.

- Virtually all job growth since the recession continues to be in the private sector. Private sector jobs are growing at a 5.0 percent annual rate, while the number of public sector jobs is declining, led by losses in federal jobs here and around the region.

- Overall, high-wage jobs have outperformed middle- and low-wage jobs since the recession. Because middle- and low-wage sectors are now well into recovery, in the past year, jobs in middle- and low-wage industries have grown faster than high-wage jobs.

-

Biotechnology

continues to be a star performer, but other high-tech

sectors also shine. The County

is outpacing the state and region in growth in biotechnology,

electronic and instruments manufacturing, and telecommunications.

High Tech jobs growing at 5% Rate - The County continues to trail the region, state and nation in information technology jobs. These sectors are engines of growth for other localities. The County has also lost jobs in the aerospace and research and testing services sectors.

- The County is home to one-third of the state's high-tech jobs. Montgomery County is also home to 90 percent of the state's jobs in high-wage industries (industries that pay an average of $50,000 per year per job).

{kind=link}

{kind=link}

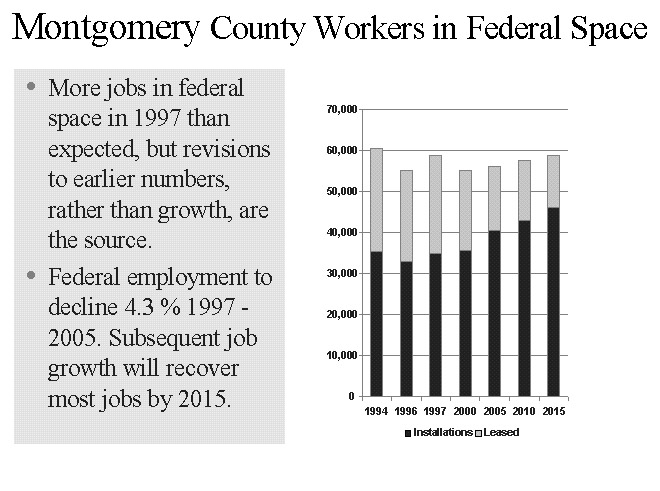

Impact of Federal Employment and Procurement

-

Jobs

at federal installations in Montgomery County increased

by 3,567 between the summer of 1996 and the summer of

1997, reflecting revisions to agency totals rather than

actual growth. In this year's survey, two federal agencies reported

a total of 3,749 additional jobs in Montgomery County.

These were job located in the County in previous years

but not reported as such by the agencies.

Montgomery County Workers in Federal Space - The

amount of federally-leased space in the County did not

change between 1996 and 1997. The amount of County space leased by

the federal government will likely decline in the future,

replaced by County space owned by the federal

government. The FDA and NIH are two prominent examples.

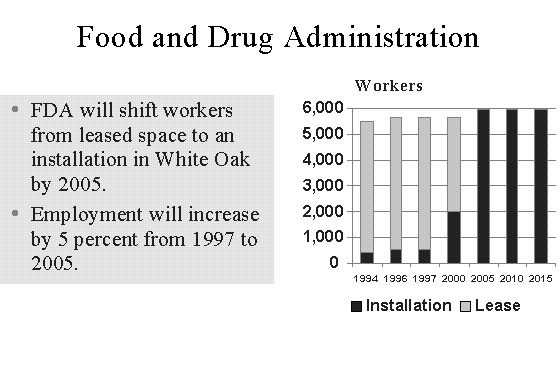

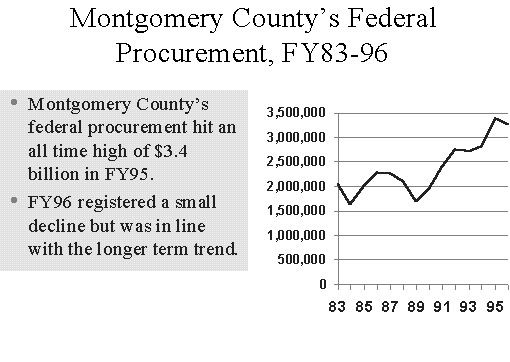

Food and Drug Administration - Federal

procurement dollars spent in Montgomery County declined

from $3.39 billion in FY95 to $3.26 billion in FY96. The decline is modest considering that in FY96 there

was a federal shutdown and a blizzard which suspended

government activity for most of the month of January

and considering that the previous year saw a huge ($400

million) increase.

Montgomery County's Federal Procurement, FY83-96

{kind=link}

{kind=link}

{kind=link}

Commercial Space Characteristics

- The region's commercial real estate market has moved from the recovery to the expansion stage. New construction is warranted and under construction in several jurisdictions.

- Most

Montgomery County submarkets are doing very well and

all are improving. Continued job growth

and limited new construction have driven vacancy rates

down and rental rates up. New office development is

expected in the Bethesda, North Bethesda, and Roockville

submarkets.

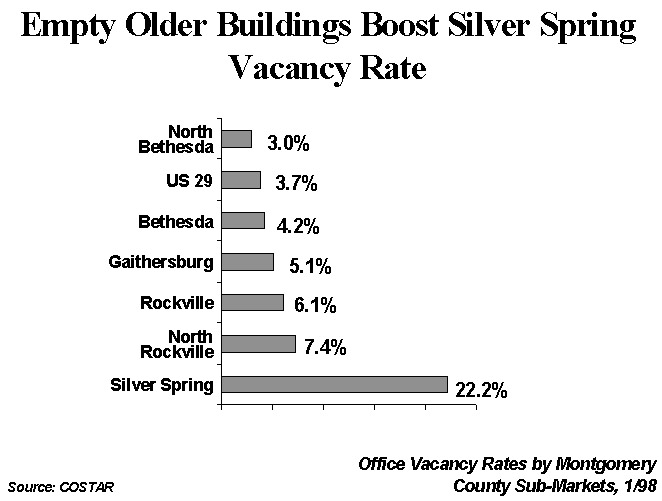

Empty Older Buildings Boost Silver Spring Vacancy Rate - The lack of high-quality "Class A" vacant space is having a positive effect on the leasing of suburban Class B space. Improvement in the Class C space market is marginally positive. Renovation of Class B buildings (and to some extent, Class C buildings in preferred locations) will continue.

- The office market will remain strong for at least 2-3 years. The flex/industrial markets are also tight, with strong demand and vacancy rates in the single digits.

{kind=link}

{kind=link}